- People

- Expertise

Our expertise

We are a team of more than 600 professionals, with the depth of experience which makes us genuine experts in our fields. Together, gunnercooke’s people have strength across just about every corporate discipline and sector. We provide legal, commercial and strategic advice that delivers real value to the clients we work with, which span from multinational enterprises through to not-for-profit organisations. Our breadth of expertise also covers specialist and emerging disciplines charity, crypto, sports and competition law.

Search by practice areaDispute ResolutionDispute Resolution OverviewMeet the Dispute Resolution TeamIntellectual Property DisputesFinancial Services & FinTech OverviewProceeds of CrimeEmployment TribunalTax InvestigationProperty Dispute ResolutionInsolvency DisputesMediationCivil Fraud & Asset TracingHealth & SafetyBusiness Crime & InvestigationsLitigation & ArbitrationInternational Arbitration - International

International Offices

The gunnercooke group has 16 main global offices across England, Scotland, the US, Germany and Austria, with further plans for growth in the coming years. These offices enhance the existing in-house capability of our dedicated international teams and dual-qualified experts that cover Spain, France, Italy, Portugal, Brazil, China, India, Poland and Hungary. Our team have clients across 126 jurisdictions, speak 46 languages and are dual-qualified in 22 jurisdictions. Our expertise means we can offer large teams to carry out complex cross-border matters for major international clients.

- Our story

Our story

gunnercooke is a top commercial law firm. We comprise a rapidly growing number of experts spanning legal and other disciplines. Clients benefit from flexible options on fees to suit their needs, access to a wider network of senior experts throughout the relationship, and legal advice which is complemented by an understanding of the commercial aspects of running a business.

- Reading Room

- News & Insights

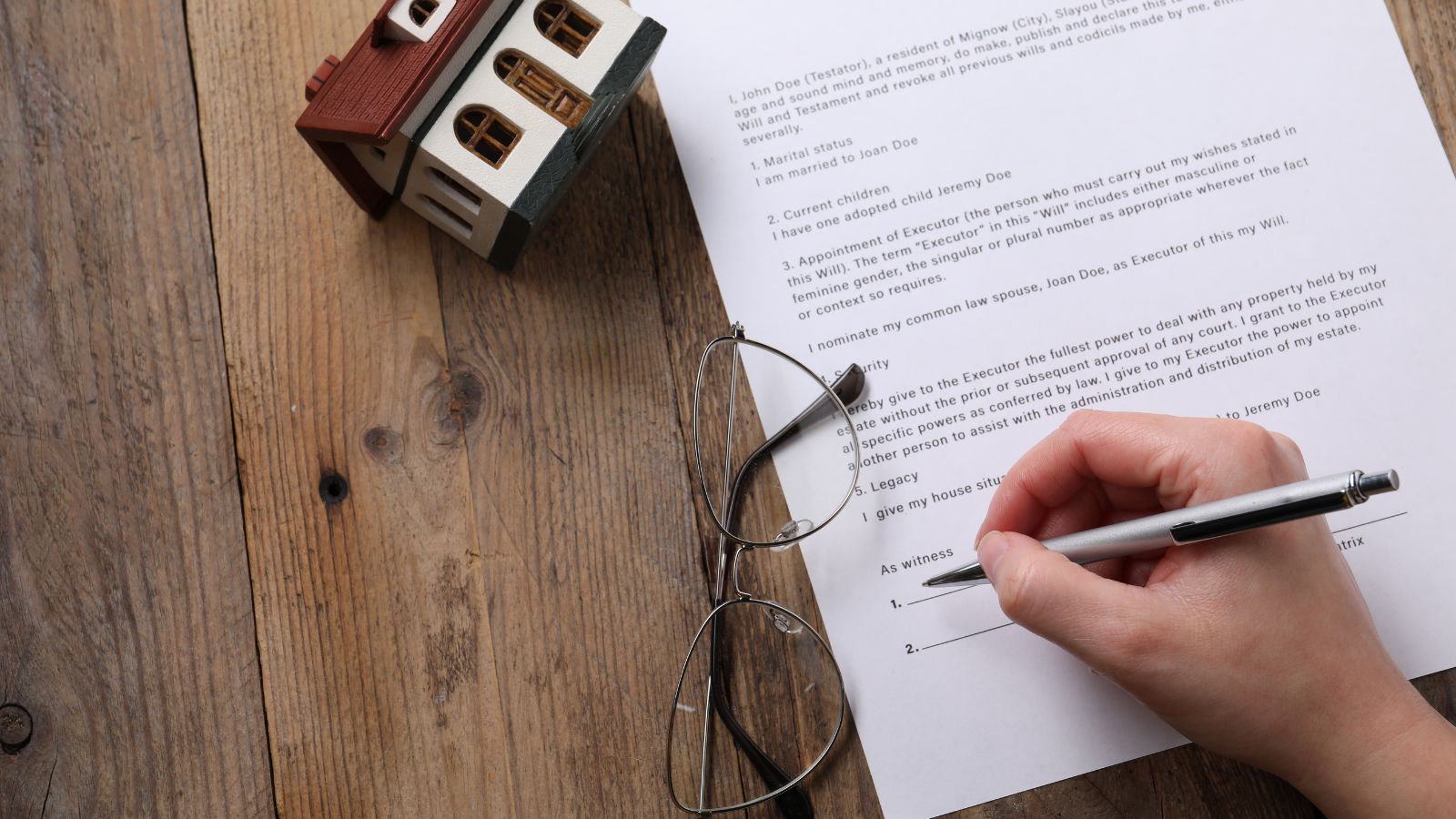

The Residence Nil Rate Band: A policy that quietly discriminates if you don’t have children

The UK’s Residence Nil Rate Band (RNRB), introduced in 2017, was framed as a targeted measure to help families pass on the “family home” to the next generation without incurring inheritance tax. It effectively increased the tax-free threshold for estates where a main residence is left to direct descendants, subject to a couple of qualifying factors. Yet beneath its simplicity lies a more uncomfortable reality: the policy systematically advantages those with children while disadvantaging those who cannot have, have lost, or choose not to have them.

At its core, the RNRB is conditional. Unlike the standard nil rate band, which applies broadly to estates regardless of personal circumstances, the additional allowance is only available when a qualifying residential interest is inherited by “lineal descendants.” This includes children, stepchildren, adopted children, and their descendants – but excludes siblings, nieces and nephews, friends, and even long-term companions who fall outside the strict definition.

The legislation introduces a structural inequality. Individuals without children – whether by circumstance or choice – are immediately excluded from accessing the full tax relief. Two estates of identical value can face markedly different tax outcomes purely based on whether the deceased had children. In effect, the tax system places a premium on a particular family structure, embedding a social preference into fiscal policy.

For those who cannot have children due to infertility or medical reasons, the exclusion can feel particularly unjust. The tax system, which is expected to operate neutrally, instead compounds an already sensitive personal circumstance. Similarly, individuals who have lost children face a harsh technicality: unless other qualifying descendants exist, they may be denied the relief despite having once met the intended “family” model, so not only have you lost a child, but the Government taxes you more as a result.

There is also a broader question of autonomy. In modern society, increasing numbers of people consciously choose not to have children. Their reasons vary – career priorities, financial considerations, environmental concerns, or simply personal preference. The RNRB implicitly penalises this choice by limiting their ability to pass on wealth tax-efficiently. It signals that some life paths are more worthy than others.

Defenders of the policy argue that its purpose is to protect the intergenerational transfer of housing wealth, particularly in the face of rising property prices. From this perspective, the focus on direct descendants is logical: it supports continuity within families and prevents the forced sale of homes. However, this rationale does not fully justify the exclusion of other forms of meaningful relationships. Many individuals without children still have dependants or close relatives who play equivalent roles in their lives.

Moreover, the RNRB adds complexity to an already intricate inheritance tax system. Its tapering for larger estates over £2m, interaction with downsizing provisions when a house is sold for a smaller one, and strict eligibility criteria create confusion and planning challenges. This complexity disproportionately affects those who do not fit the “standard” family model, as they must navigate a system that offers them fewer straightforward benefits.

There are alternatives. A more equitable approach could involve extending the relief to a broader category of beneficiaries or integrating the RNRB into a single, higher nil rate band applicable to all estates regardless of familial status. Such reforms would preserve the policy’s intent – mitigating inheritance tax on primary residences, while removing its discriminatory edge targeted at those who do not have children, through a choice or otherwise. In a diverse society where family structures and personal choices vary widely, tax rules that privilege one group over another are outdated, unjust and, in my view, discriminative.

As debates around inheritance tax continue, the RNRB deserves closer scrutiny – not just for its fiscal impact, but for the values it encodes in a modern day society. A fair tax system should not hinge on whether someone has children. Yet, in its current form, that is precisely what the Residence Nil Rate Band does.

If you would like to learn more, you can contact Amy Lane here for expert legal advice.

To receive all the latest insights from gunnercooke to your inbox, sign up below